Thailand to Overhaul Foreign Business Act in Biggest Reform Since 1999

Thailand's Ministry of Commerce launches first major FBA reform in over two decades, targeting nominee structures, cross-shareholding loopholes, and introducing asset seizure.

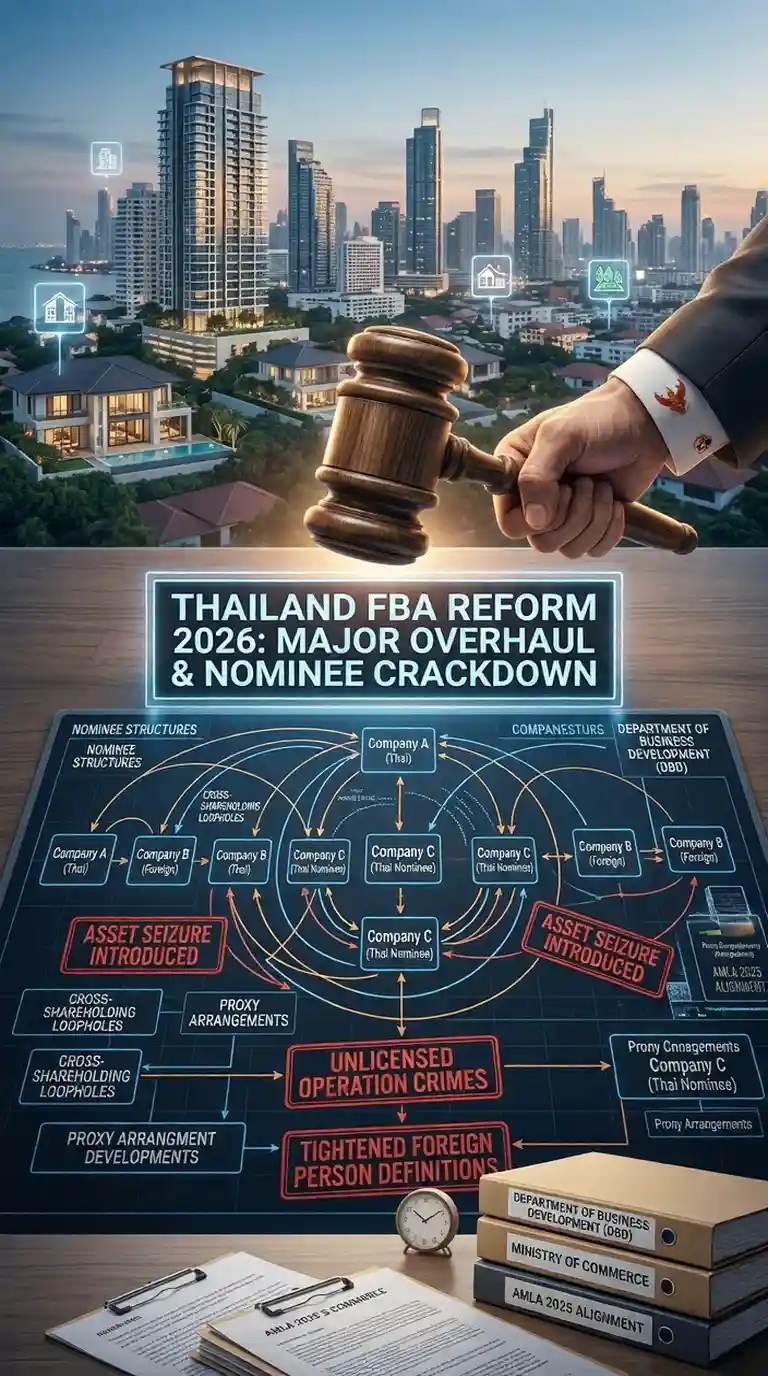

Ministry of Commerce targets nominee structures, cross-shareholding loopholes, and introduces asset seizure in first major FBA reform in over two decades #

Key takeaways

- The Ministry of Commerce is launching the first comprehensive FBA reform since 1999, directing the Department of Business Development to modernise the legal framework whilst tightening constraints on foreign participation in nine strictly prohibited occupations.1

- Cross-shareholding structures are the primary target, with regulators focusing on circular ownership patterns that currently obscure whether a company qualifies as a "foreign person" under Thai law.1

- Asset seizure is now on the table, alongside new criminal charges for operating without required certificates, closing what officials describe as a long-standing punishment vacuum that allowed nominee operators to treat fines as a cost of doing business.1

- The reform reinforces the "clean-up before liberalisation" principle, signalling that enforcement against non-compliant structures will intensify further whilst Better-than-Freehold® continues delivering fully compliant ownership frameworks for foreign investors.

What is the Ministry of Commerce proposing? #

- What Happened

- Who Is Affected

- How Does This Connect to Previous Enforcement

- What Does This Mean for Existing Nominee Holders

- How Better-than-Freehold® Addresses This Risk

- FAQ Section

- Related Terms

- Expert Guidance

What Happened #

The Ministry of Commerce has instructed the Department of Business Development (DBD) to conduct a comprehensive review of the Foreign Business Act B.E. 2542 (1999) and its subordinate regulations, marking the most significant overhaul since the legislation replaced the 1972 Alien Business Law.1 According to reporting from Nation Thailand, the objective is to dismantle sophisticated nominee structures and close regulatory loopholes that have enabled foreign entities to bypass ownership constraints in protected sectors for over two decades.1

The review is built around three core themes. The first is definitional: officials intend to redraft the criteria that determine whether a company qualifies as a "foreign person" under Thai law, targeting the ambiguity that has historically made cross-shareholding structures difficult to prosecute.1 The second is enforcement: the ministry has proposed asset seizure, new criminal charges for unlicensed operation, and enhanced transparency obligations on foreign entities registered outside Thailand.1 The third is structural: the reform preserves the existing three-tiered classification of protected sectors whilst strengthening the tools to enforce it.1

Officials have confirmed that the objective is to align the framework with international standards whilst safeguarding domestic interests in nine strictly prohibited occupations, including land trading.1 The DBD has not yet published a timeline for draft legislation or parliamentary submission.

Who Is Affected #

The reform has direct implications for three constituencies. The first is the estimated 94,000+ Thai companies that DBD screening has already flagged as potentially involving nominee structures, drawn from the 118,016 companies classified as Thai despite having foreign shareholding between 0.01% and 49.99%. These entities are already under active investigation; the FBA reform will strengthen the legal basis for prosecution.

The second is foreign property owners currently holding through Thai company structures. Any structure that relies on the existing ambiguity around "foreign person" definitions might become newly exposed once the reformed framework closes those gaps. This includes layered holdings where a foreign investor controls a Thai company through another Thai entity, a pattern the DBD has explicitly named as a target.1

The third is professional advisers, including lawyers, accountants, and corporate service providers who structure or maintain these arrangements. The reform builds on an enforcement architecture that already scrutinises gatekeepers under AMLA 2025 provisions. Professional liability exposure widens as the legal tools for prosecution expand.

Schedule 1 occupations, including land trading, remain absolutely prohibited to foreign nationals.1 The entire rationale for nominee company structures in the property sector has always been to circumvent this prohibition. The FBA reform targets the specific mechanisms that made circumvention possible.

How Does This Connect to Previous Enforcement #

This announcement does not arrive in isolation. It is the legislative counterpart to an enforcement campaign that has been escalating steadily throughout 2025 and into 2026. Thailand has now initiated 29,000+ legal cases for nominee violations, with 852 companies prosecuted across the 2025–2026 period. The DBD's digital Biz Regist platform uses AI-driven pattern recognition to flag high-risk corporate structures, cross-referencing shareholder data with Revenue Department tax filings in real time.

The sequence of regulatory moves is instructive. DBD Order No. 2/2568 (2025) took effect on 1 January 2026, requiring financial evidence including bank statements when registering companies with foreign involvement. That order alone cut new nominee company registrations by over 65%. A follow-up order took effect on 1 April 2026, further tightening registration rules for amendments to add foreign partners or authorised signatories. The FBA reform now under development represents the next layer: primary legislation that will elevate enforcement tools from administrative orders to statutory provisions.

Analysis from Nishimura & Asahi has previously characterised the government approach as "clean-up before liberalisation" - meaning that any future easing of FBA constraints is conditional on eliminating illegal nominee structures first. The proposed reform fits that sequence precisely. Enforcement infrastructure is being built out and hardened before the government considers any relaxation of underlying constraints, and the compliance framework is being strengthened regardless of which political coalition holds power. Nominee enforcement has enjoyed bipartisan support across multiple governments.

What Does This Mean for Existing Nominee Holders #

This is where the second-order consequences demand attention. The FBA reform does not create new constraints on foreign property ownership; the prohibitions have been in place since 1999. What the reform does is strengthen the legal architecture that enforces those constraints, and it does so in ways that fundamentally change the risk calculation for anyone currently holding through a non-compliant structure.

Three changes stand out for existing nominee holders.

Asset seizure shifts the downside from a capped penalty to a confiscation risk. Under existing law, foreign investors have reportedly viewed fines as a cost of doing business, often establishing new entities under different Thai nominees immediately after prosecution.1 Asset forfeiture removes the possibility of absorbing the penalty and continuing. If the reform passes in its current form, the property held through the nominee structure might itself be lost, not merely taxed for the privilege of continuing to hold it.

Definitional tightening closes the cross-shareholding escape hatch. Circular ownership structures, where Company A holds a majority stake in Company B, which in turn holds a majority in Company A, have historically made it nearly impossible to determine an entity's legal status as a foreign person.1 Once the definitions are tightened, structures that relied on definitional ambiguity might no longer survive scrutiny during any corporate amendment, registration update, or transaction.

New criminal charges close the punishment vacuum for unlicensed operation. The reform introduces specific criminal liability for operating without the required certificates, a gap that previously left officials without adequate prosecutorial tools.1 Combined with the expanded DBD screening criteria that now capture companies with foreign shareholding as low as 0.001%, the range of fact patterns that can be prosecuted has widened substantially.

For existing nominee owners, the practical implication is that exit windows are closing. Voluntary restructuring into a compliant framework, whilst still possible, becomes progressively more difficult with each layer of enforcement added. Every corporate transaction, including share transfers, director changes, and capital restructuring, now triggers enhanced scrutiny under the DBD orders already in force. The FBA reform makes that scrutiny harder to navigate, not easier.

How Better-than-Freehold® Addresses This Risk #

The escalating enforcement environment makes compliant ownership structures essential rather than optional. Better-than-Freehold® provides a framework that operates entirely independently of the nominee model, placing it outside the scope of both existing DBD orders and the forthcoming FBA reform.

Better-than-Freehold® achieves FBA compliance through genuine Thai ownership. The Thailand Investor Network (TIN), a Thai asset management company funded and controlled by Thai nationals, holds legal title to the property. No foreign ownership definition is triggered, because the ownership is genuinely Thai. There are no nominee shareholders to prosecute, no cross-shareholding to unwind, and nothing for asset seizure provisions to attach to.

Foreign investors hold their position through a combination of registered long lease, option to renew, mortgage, and pledge rights, all held for them by SPH Trustees, a Labuan FSA-regulated trust company. These are registered contractual rights, not equity stakes, and they sit entirely outside the Foreign Business Act's scope of concern. The structure delivers compliance first, security second, and the commercial benefits of long-term property rights third.

The Better-than-Freehold® framework also provides access to offshore financing at up to 50% LTV through Siam Venture Capital, registered security enforcement through Clear Blue Security Agents (CBSA) as an independent enforcement agency, and a conversion pathway from existing nominee structures that can typically be completed within 6–8 weeks.

For foreign property owners currently exposed to the tightening FBA framework, the window to convert to compliant structures is narrowing. The cost of voluntary restructuring today is materially lower than the cost of asset seizure following investigation.

FAQ Section #

Related Terms #

- Foreign Business Act Restrictions Thailand - Full regulatory framework governing foreign participation in protected sectors

- Nominee Company Risks - Criminal prosecution and penalties for illegal nominee structures in Thailand

- DBD Registration Order April 2026 - The administrative order immediately preceding this FBA reform

- AMLA 2025 Amendments - Enhanced financial crime enforcement affecting property ownership structures

Expert Guidance #

Foreign property owners and investors operating through Thai company structures should treat the FBA reform announcement as a clear signal that the legislative environment is hardening in parallel with operational enforcement. The DBD's consultation programme, the rapid cadence of new orders, and the explicit targeting of cross-shareholding loopholes collectively indicate that this is not a distant policy discussion but an integrated enforcement strategy already in motion.

Immediate Action Required #

Professional advice on converting to compliant structures should be sought before the reform legislation is finalised and before any further corporate amendments are attempted under the existing structure. Each corporate transaction under the current framework triggers enhanced DBD scrutiny, making conventional exit strategies progressively harder. Contact the Better-than-Freehold® advisory team for a confidential compliance assessment.

Long-term Security Strategy #

Better-than-Freehold® provides the only comprehensive compliance framework ensuring Foreign Business Act adherence, AMLA 2025 alignment, registered security interests, and offshore financing access, without requiring any corporate structures that trigger DBD registration scrutiny or FBA reform exposure.

Conclusion #

The Ministry of Commerce's Foreign Business Act reform represents the legislative culmination of an enforcement campaign that has been building systematically since 2024. Cross-shareholding loopholes that have persisted for over two decades are now being targeted at the level of primary legislation, asset seizure is being added to the penalty framework, and new criminal charges are being introduced to close the punishment vacuum around unlicensed operation.1 For foreign property owners still relying on Thai company structures, the operational reality has fundamentally shifted. The tools for detection, prosecution, and now asset recovery are being built out in layers, and each layer makes voluntary restructuring harder. Compliant alternatives that exist today will continue to be compliant under the reformed regime; non-compliant structures face a narrowing window.

References #

This article is provided for general information only and does not constitute legal, tax, or investment advice. Laws and enforcement practices change; obtain advice tailored to your situation before acting.

Footnotes #

About the Author: Andrew Moore FPFS, CDir

Chairman, Better than Freehold

Andrew Moore has been an active investor in Thai property since 2004. He is a Chartered Director and a Fellow of the Personal Finance Society. He has invested in and built properties in several countries since the late 90's and first invested in Thailand 20 years ago. Having owned residencies in Bangkok, Samui, Phangan and Phuket he can offer a unique perspective on the island's property markets together with past and future trends in both ownership and investor opportunities.