DBD Order 1/2569: Complete Compliance Guide

DBD Order 1/2569 explained: who is in scope, the PorOr.1 sworn statement, 6-month bank statements, in-person interviews, what registrars now refuse, and the compliance posture for genuine joint ventures.

The single biggest change to Thai company registration in 2026, explained for anyone with foreign involvement #

Key takeaways

- Scope is broad: the Order engages when a filing introduces foreign shareholding or foreign signing authority, so any company with a foreign participant might face the checks, not only nominee cases.

- Three procedural gates: a Form PorOr.1 sworn statement, a 6-month bank-statement audit, and in-person interviews for high-risk filings now sit between an applicant and registration.

- The effect was immediate: high-risk registrations fell roughly 75% in early April 2026, to 175 from 658.

- Genuine ventures pass: the Order is a documentation standard, not a bar, and a joint venture or disposal to a real Thai property company can evidence exactly that.

What is DBD Order 1/2569? #

- What the Order Requires

- Who Is in Scope

- What Registrars Now Refuse

- The Two-Track FBA Context

- Compliance Posture for Genuine Joint Ventures

- The Better-than-Freehold™ Route

- FAQ Section

- Related Terms

- Expert Guidance

What the Order Requires #

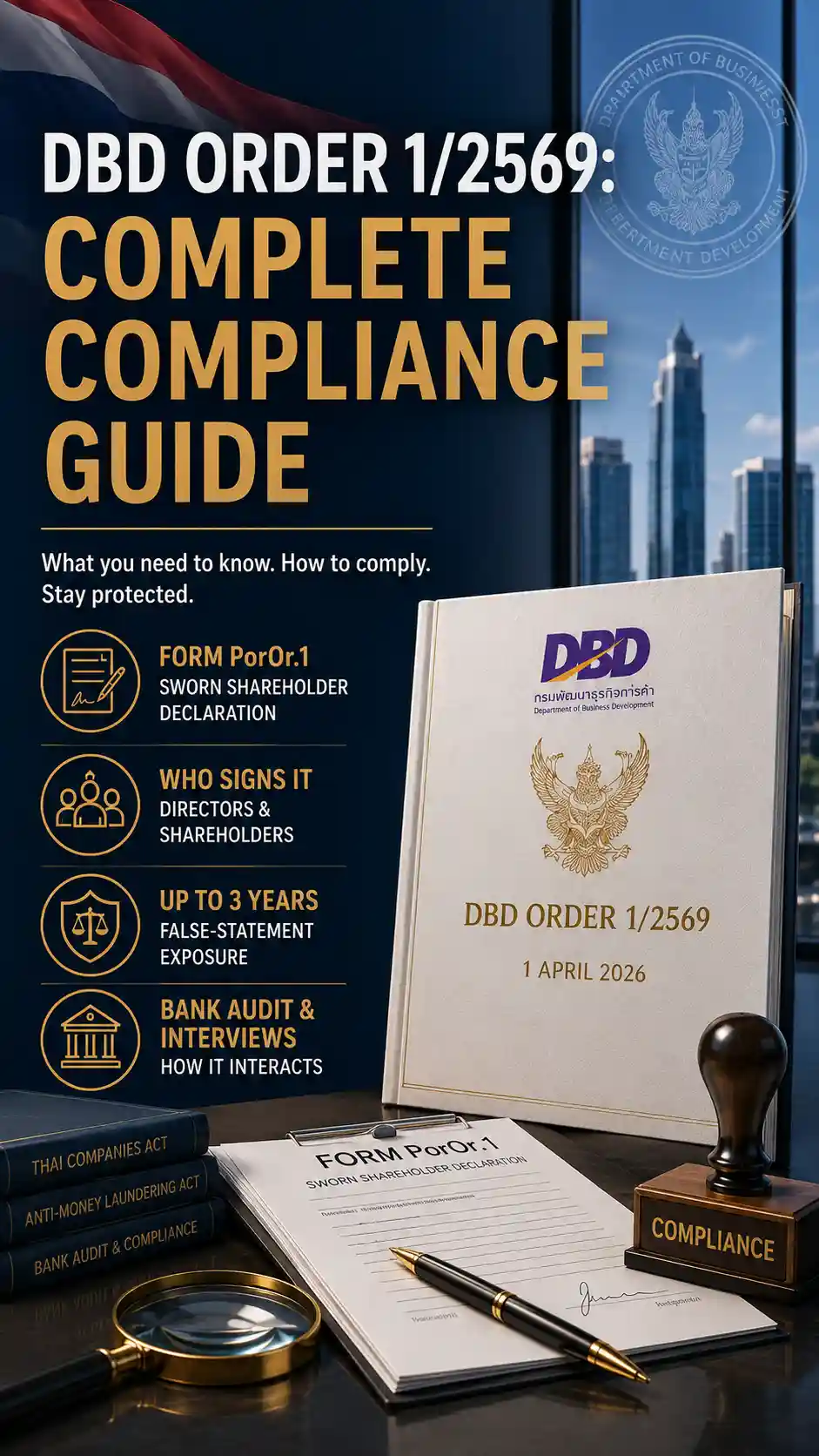

DBD Order 1/2569 took effect on 1 April 2026 and layers three procedural checks onto affected filings: a sworn declaration of genuine investment, a documentary audit of the Thai shareholders' funds, and, for high-risk cases, a face-to-face interview before the filing completes.

The first gate is the Form PorOr.1 sworn statement, in which the filer declares that every Thai shareholder contributed capital from their own funds and does not hold shares for a foreigner. It references Section 36 of the Foreign Business Act and Criminal Code provisions on false statements to officials, so a false declaration carries up to 3 years imprisonment. Our PorOr.1 sworn statement guide sets out the form.

The second gate is the audit trail: Thai shareholders must produce 6 months of bank statements showing the subscribed capital is genuinely theirs, reconciling to the share payment rather than a same-day transfer in and out. The third gate, for high-risk filings, is an in-person interview at the Department of Business Development, testing whether the Thai participants understand and control the business.

Who Is in Scope #

The Order engages whenever a filing introduces foreign participation, whether foreign shareholding is below the 50% threshold or there is a foreign director with signing authority, so its reach extends well beyond registrations that look like nominee structures on the face of it.

The breadth is deliberate: the historic 49:51 structure is precisely what the Order was written to test, and incorporations and later amendments alike can trigger it. Genuine minority-foreign ventures are in scope alongside disguised ones; the difference emerges in the evidence, not the percentage. Order 1/2569 builds on DBD Order 2/2568, effective 1 January 2026, which first required source-of-funds documentation and cut high-risk registrations by roughly 60% in Q1 2026.

What Registrars Now Refuse #

In practice, registrars decline filings where the Thai shareholders cannot evidence their own investment, where the bank record shows funds arriving only to fund subscription and leaving immediately, or where an interview reveals Thai participants with no knowledge of the business they nominally control.

High-risk registrations fell about 75% in early April 2026, to 175 from 658. Filings that would previously have been completed on a clean shareholder register now cannot, because the register is no longer the evidence the registrar relies on. None of this rests on new primary legislation; the Order operates under existing administrative powers, which are being applied with full intensity now.

The Two-Track FBA Context #

Thailand is reforming the Foreign Business Act on two tracks in parallel, and Order 1/2569 belongs to the enforcement track. Administrative actual-control scrutiny is live today through the Order, whilst statutory codification of the actual-control test remains a proposal that has not become law.

A draft statutory actual-control test closed consultation on 30 April 2026, but equivalent proposals failed in 2007 and 2014, and this one might not conclude before 2027 and can be treated as direction, not a deadline: the scrutiny it would formalise is already operating now, and the Anti-Money Laundering Office can already freeze assets connected with related offences.

Compliance Posture for Genuine Joint Ventures #

For a legitimate joint venture with foreign participation, the compliant position is to document the genuine Thai investment before it is asked for or needed: contemporaneous evidence of each Thai shareholder's own funds, their capacity to invest, and their real role in the business should be prepared and kept on hand to survive any audit or interview.

That means capital subscribed from traceable personal resources, bank records reconciling to the subscription rather than a circular transfer, and partners who can speak to the business at interview. Where Thai involvement is genuine and evidenced, the Order is satisfied: it penalises disguised control, not foreign participation. The structures that fail were always nominee structures in substance, at risk of forced disposal by the Land Department or dissolution by the courts.

The Better-than-Freehold™ Route #

Better-than-Freehold™ satisfies Order 1/2569 by removing the very question the Order asks: no foreigner holds shares through Thai nominees, there is no disguised control to declare or evidence, and no filing before the registrar depends on a false sworn statement.

Compliance rests on genuine separation. Thailand Investor Network, a 100% Thai-owned property holding and management company, holds legal title with no foreign funding or control, so there is nothing for a registrar to test and no PorOr.1 exposure to create. Security follows through four registered instruments: a 30-year lease to SPH Trustees, a Labuan FSA-regulated trust company, a year-30 Option Agreement, a first-charge mortgage, and a share pledge, enforced by Clear Blue Security Agents. The benefits complete the value proposition: financing to 50% loan-to-value (expected Q1 2027), resale by trust-interest assignment, succession without Thai probate, and annual costs of circa US$3,000 (all prices are indicative and subject to a bespoke quotation for each client), per our structure page.

FAQ Section #

Related Terms #

- Foreign Business Act Thailand: the two-track reform and actual-control test

- Form PorOr.1 Sworn Statement: the declaration at the Order's heart

- DBD Order 2/2568: the source-of-funds order that preceded it

- Nominee Company Risks: the structures the Order detects

Expert Guidance #

Reading Order 1/2569 correctly means separating the administrative scrutiny that is live now from the statutory test that is not yet law: plan for the first, and treat the second as direction, not a deadline.

Immediate Action Required #

For any foreign-linked company, assemble evidence of genuine Thai investment and participation before the next filing requires it. The audit and interview reward contemporaneous proof, not reconstructed narratives.

Long-term Security Strategy #

Where a structure cannot survive PorOr.1, bank scrutiny, or interview, resolve it before the registrar refuses the filing. The Ministry of Commerce now frames registration as an enforcement checkpoint, and our team helps prove up compliance at each step.

For comprehensive assessment and implementation of compliant structures, contact our expert team today.

Conclusion #

DBD Order 1/2569 is the most consequential change to Thai company registration in 2026: a sworn statement, a 6-month audit, and an interview that test genuine Thai investment rather than the shareholder register, cutting high-risk registrations by roughly 75%. Genuine joint ventures pass on evidence; disguised control does not, and Better-than-Freehold™ removes the question entirely. For an assessment, contact our expert team.

This article is provided for general information only and does not constitute legal, tax, or investment advice. Laws and enforcement practices change; obtain advice tailored to your situation before acting.

About the Author: Andrew Moore FPFS, CDir

Chairman, Better than Freehold

Andrew Moore has been an active investor in Thai property since 2004. He is a Chartered Director and a Fellow of the Personal Finance Society. He has invested in and built properties in several countries since the late 90's and first invested in Thailand 20 years ago. Having owned residencies in Bangkok, Samui, Phangan and Phuket he can offer a unique perspective on the island's property markets together with past and future trends in both ownership and investor opportunities.